In the conventional finance model, a central institution, such as Bank of America, provides capital and decides which borrowers qualify for loans. In the peer-to-peer model, individual people brought together by the power of the Internet, in an aggregate known as “the crowd,” provide the capital and make the underwriting decisions.

P2P lenders cover a spectrum, depending on how you define them. In a TechCrunch article titled “The State of P2P Lending” published this year, author Sonny Sign suggests that any online lender is a P2P lender, although that’s a strange definition in my book. More-mainstream definitions would classify a company such as Prosper as a prominent P2P lender. But even in that case, a P2P purist could challenge in at least a couple of ways the extent to which such a company is truly P2P.

P Is For…

Firstly, while Prosper began by sourcing capital primarily from individual investors or peers, these days it increasingly sources its capital from institutional investors. According to an analysis published by Risk.net, asset managers, banks, and hedge funds made around two-thirds of the loans that originated on Prosper in 2014. While many peer investors remain on the platform—including myself—it now seems to make the majority of its loans from hedge fund to consumer rather than P2P.

Secondly, whereas Prosper previously allowed investors to see the peers they were investing in, it now anonymizes the website. During the 2007 Finovate, a conference showcasing innovations in finance and technology, Prosper cofounder Chris Larsen debuted a platform where investors could see a picture of whom they were lending to. Today, loan listings no longer identify such information. Of course, investors are still choosing which people they are lending to, but there is no personal connection between lenders and borrowers.

Prosper is a great company, and I am a very satisfied investor. Prosper is enabling American consumers to access capital at lower rates than conventional sources, and it has seen phenomenal growth and success. I am simply pointing out that one might question the extent to which it facilitates true P2P connections on its platform.

Encouraging Personal Connection

Of course, I am highly biased; as senior director for Kiva Zip, I believe our model represents an even truer vision of P2P lending. While we do source some capital from institutional lenders including Capital One, Deutsche Bank, and the MetLife Foundation, the vast majority of our money comes from individuals like you and me. Kiva Zip’s institutional capital partners play more of an amplifying role, generously matching loan amounts initiated by the crowd.

Even more important to us is not just allowing but positively encouraging personal connections between borrowers and lenders on our platform.

When we launched Kiva Zip in Newark, New Jersey, we made a loan to Vaughn and his business, Living Adventure Tours. Vaughn takes people kayaking, biking, and adventuring in the outdoors, and all of his guides are returning veterans. In an outpouring of support that was wonderful to witness, 143 lenders crowdfunded Vaughn’s loan. One Kiva lender commented, “As a veteran myself, I value individuals such as yourself who recognize and respect those coming home. Thank you for all you are doing. Keep up the good work.” Another supporter wrote, “I am making this loan in honor of my beloved nephew Colton who passed away six and a half years ago. Today is his birthday, and I think he would have really enjoyed your program and business concept. Many happy adventures to you and your adventurers!”

For our team, the personal connections, generosity, and empathy that P2P lending can engender are not peripheral; they are core to our ethos and mission. In a recent survey of Kiva Zip borrowers, over half told us that they had seen an increase in customers as a result of borrowing money on our platform. And while success in small business is partly about access to capital, it is also about access to customers and connections. Our hope is that by connecting our borrowers with hundreds of enthusiastic and passionate lenders, we can help provide access to all three.

On Vaughn’s Kiva Zip loan page, you will see a link to his business’s website, Facebook page, Twitter page, and Yelp profile. You will also see a “Conversations” tab where Vaughn’s lenders and would-be lenders can ask him questions, as well as give him ideas and advice. In part, this is about promoting personal connections between the borrower and its lenders, but it is also about encouraging a more democratic approach to underwriting loans.

Who’s Underwriting?

In the Prosper model, when an investor—whether an individual or a hedge fund—makes a loan, that investor is almost certainly relying on Prosper’s algorithm to assess the riskiness of the loan (that is, AA rating for lowest risk, A for next lowest, and so on). That algorithm is objective, inflexible, and centralized. This process undermines the Prosper investor as the underwriter.

In the Kiva Zip model, we empower our community to democratically underwrite loans and decide which ones get funded. Where an inflexible algorithm might make a black-and-white decision to reject a small farmer’s loan application because he has insufficient cash flow or collateral, 200 out of our million-strong lender community might stand up and say yes to that same farmer’s loan because they care about the cause of small-scale, sustainable agriculture, or because the investor has known the farmer personally for over a decade, and puts more emphasis on that personal relationship than on other financial factors.

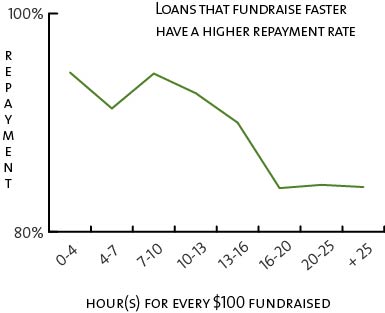

This crowdsourced, flexible, subjective, and human-centered approach to underwriting allows us to expand access to capital for entrepreneurs that conventional financial underwriting would disqualify. And our data suggests that it can also be effective from a risk management perspective. Figure 1 shows that the loans that fundraise most quickly on Kiva Zip tend to have the highest repayment rate and vice versa—there is wisdom in the crowd!

P2P lending covers a spectrum of different offerings. I believe the truest P2P lending models source capital from individual people, and empowers them to democratically decide which borrowers get funded based on their own personal preferences and passions. And by personally connecting investors with the borrowers, their funding supports enterprises not just with financial capital, but with social capital as well.

Jonny Price is a graduate of the University of Cambridge, where he majored in history. After six years at Oliver Wyman, he joined Kiva in September 2011. Jonny is married to Ali, and lives in San Francisco.