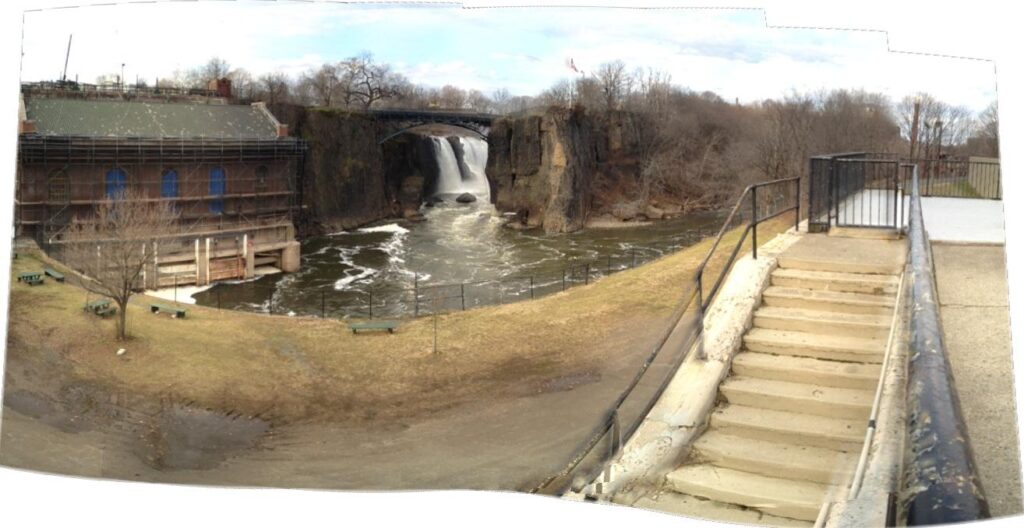

At the newly created Paterson Great Falls National Historic Park on the Passaic River in northern New Jersey, there stands a sign inscribed: “Alexander Hamilton envisioned the great potential power of these scenic falls for industrial development.” This is nature at the service of money and the economy.

Looking around brought with it a chilling reminder of fallen industry in a town that the poetry of William Carlos Williams celebrated and economic history left behind.

Hamilton was an economic visionary. He saw nature as an underutilized economic resource and perceived the opportunities of young untapped markets. For Hamilton, fixing the major structural debt problem in post-revolutionary America’s finances by stimulating industrial manufacturing was both motivator and strategy. In 1791, Paterson became the first industrial park.

The history of Paterson’s Great Falls was about new industries including textiles (especially silk), handguns, rope, continuous sheet paper, submarines, locomotives and, later, airplane engines. With the application of capital and ingenuity, energy was extracted from the water and transformed into power, power into manufacture, manufacture into markets, markets into capital, capital into wealth, and wealth into power.

In the story of how natural resources are used for profit, between land [representing all natural resources] and money, is an economic paradigm in need of reassessment and intervention. In Paterson, what all that industry returned to the water by way of manufacturing and toxic waste was an insult to the living water and eco-system.

The polluted de-natured Passaic flows on as a man-made emblem of what happens when capital or money is extracted from nature without regard for nature’s regeneration; in essence, nature is left to die. Capital moves freely about the world, across space and time; land and natural resources are rooted in place and geologic time. In a materialistic economy, time is money, and money used in this way sadly has no patience for the evolutionary pace of nature.

Hamilton knew the need for natural resources of all kinds would increase continually to support economic and national development. He could see no limits to economic growth, and along the way contributed to what would become the industrialization and commodification of everything, including agriculture. With the emergence of property rights granted to individuals and corporations by the government, the mutuality of “ownership” in common gave way to the self-interest characterized so ably by Adam Smith in The Wealth of Nations, first published in 1776, the same year as the Declaration of Independence was signed. The drive of self-interest is deeply connected to accumulations of wealth.

Numerous economists have observed the cyclical patterns of boom and bust, the disparity of wealth and poverty that seem an endemic part of the industrialized and global economy. But, none has addressed it as directly as Henry George with the publication of Progress and Poverty in 1880. George argued that land and natural resources should be owned in the commons, and that private ownership and the control of rents was one of the major contributing causes of impoverishment of the many at the hands of the few. As a remedy, he proposed a single tax on the value of land. This tax would return to the public the monetary resources that in some senses were sequestered in the land and in private hands. What George was trying to do was find a monetary equivalent for decommoditizing the land, to make it in the community’s interest to make sure that the land was rightfully used and stewarded for future generations. George’s was a land-based economy in which the community benefited from the wealth generated by the increasing value of land.

Henry George’s approach to economics represents a view that land and all natural resources are not economic unto themselves. That is, they do not enter the economic stream until someone works on that resource; the product of that work is economic. Rudolf Steiner in his lectures on Economics given in 1922 put forth a similar concept and elaborated further that this work on the land generates one kind of value. He also identified a second kind of value stream: that which emerges when intelligence is applied to labor. These dynamically related principles lie at the heart of economic life. However, the land-based stream has been devalued as it tends toward place, and stands against the imperative of capital and global markets.

Jane Jacobs, in her study of economics in an urban environment in the late 20th century, developed a vision of self-sustaining regional economies based upon what she called import replacement. Hers was a vision of small-to-medium-scale entrepreneurs and manufacturers who would find ways to make things based upon regional natural resources. She indicated that this approach would also reduce the environmental degradation that results from extensive transportation of goods. Her vision also includes that which Hamilton missed—a mindfulness of organic systems that finds innovative ways to transform waste into new value.

Each of these visionary economic thinkers saw the economy as a whole system, and brought a new perspective based upon the reality of their respective times. The purpose of narrating these various views of land and money is to tease out of them some sense of how we can actually live in a dynamic tension between the two, and to resurrect the shared reality and importance of land and natural resources, not as economic in and of themselves, but as part of a livable economic future—and before it is too late to do so.

The money economy is global. It allows for trade and the movement of manufactured goods across political boundaries, and money can move around the world at electronic speed. It supports scale and efficiency and has made the accumulation of wealth a bedfellow of unparalleled poverty. It has, unfortunately, pervaded all aspects of economic life to the exclusion of other ways of being economic.

The scale and consequences of recent events indicate an unhealthy disconnect between money and land to the extent that land itself has become a treasury measured in ever-rising prices, which, in turn, have presented barriers to access, especially for farmers. In the land economy, people are connected to what is made from it, and to the soil and to stewarding the resources themselves.

We need both facets of the economy, but with a renewed awareness of land. By and large the land economy has been adumbrated by the money economy. Everything, it seems, has been monetized. What numerous contemporary movements are doing is trying to reawaken the local-regional land-based economy consciousness. In essence they are encouraging communities and individuals to take back authority for the development of economic life out of a sense of interdependence.

We need an economy that raises the land-based on equal ground with the global, recognizes the value and role each play, and manages capital in a way that supports the interplay between them. To change our economic being will require a radical reconsideration of ownership—how we own, why we own—and a major disruption of the myth of self-interest. The reality of our interdependence in economic life will celebrate the importance of community-interest, both local and global. But nothing will happen in this direction unless each of us steps out of self-interested consumer-owner consciousness—one endgame of the money economy—and finds a way to really reconnect with land, not as real estate, but as the source of life.

By John Bloom

John Bloom is the former Senior Director of Organizational Culture at RSF Social Finance